Welcome to J Insurance Blog. J Insurance is an online commercial insurance provider. We provide all types of business insurance catered to your business’s specific needs. We are a one-stop solution for low-cost insurance products and we take care of everything for you, starting from recommending you the best policy all the way to handling your claims and their disbursement.

Today, we are going to tell you all that there is about insurance so that you can know “What is Insurance”?

So, what is insurance?

Insurance is ideally a contract between two parties, portrayed as a policy so that one party is able to provide financial protection to the insured party against the unwanted financial risks and contingencies.

They are basically hedging instruments that can be used to insure mostly anything of value, irrespective of its risk or liability to cover the damage.

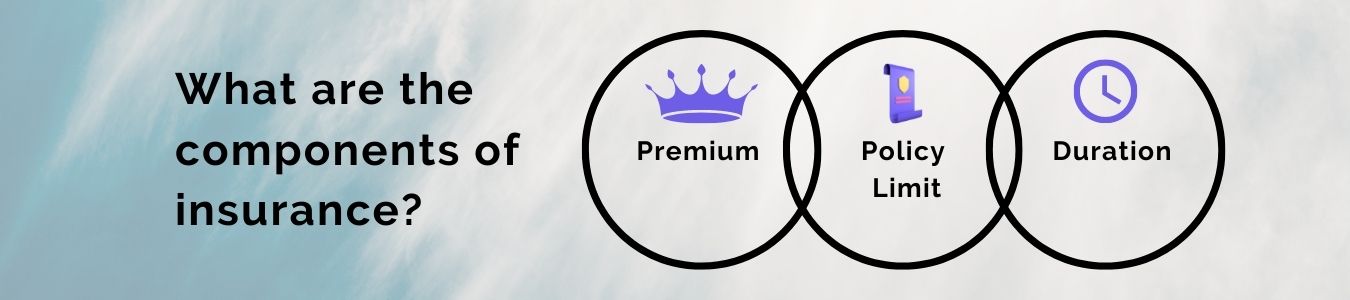

What are the components of insurance?

If you’re someone who is considering buying insurance then you should be well-informed about all the things that are there related to it. A good understanding of all the concepts related to insurance will make sure that you make the right decision when you buy an insurance policy either for yourself or your business.

So there are essentially 3 major components to insurance.

- Premium

- Policy Limit

- And Duration

Premium is basically the price of buying the insurance policy. It can be expressed as an annual cost. The premium amount is decided as per your risk profile.

The policy limit is the maximum amount that you are eligible to be covered for or you can say it is the maximum amount that the insurer will bear in case of claim settlement. It is also called Sum Insured.

The duration of the policy signifies the time period for which the policy will be applicable.

So how does insurance work?

So companies offer insurance products and the insurers can choose from a variety of insurance policies available. People can choose from personal insurance products and commercial insurance products.

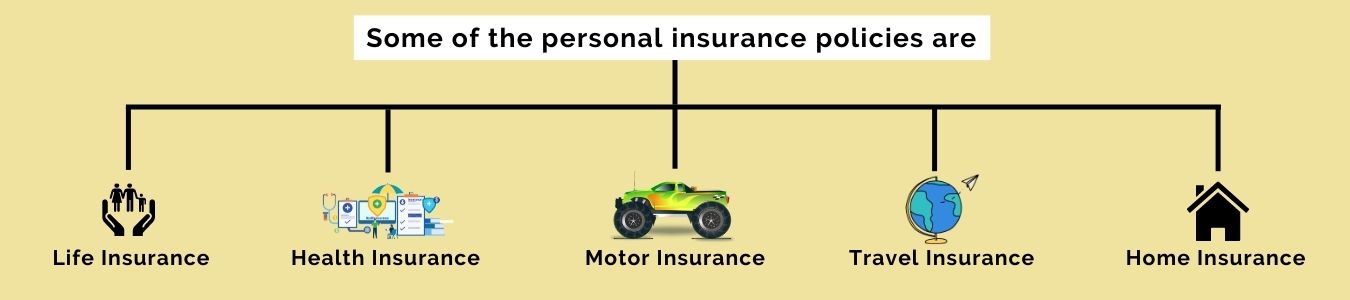

Some of the personal insurance policies are:

- Life Insurance

- Health Insurance

- Motor Insurance

- Travel Insurance

- Home Insurance

Some of the commercial insurance policies are:

- Standard Fire and Special Perils Policy (Property, Asset, Stock, Office Insurance)

- Marine Insurance (Transit)

- Group Travel Insurance

- Engineering Risk (Contractor Risk, Erection Risk, Plant & Machinery Risk)

- Workmen Compensation Insurance

- Group Health Insurance

Let’s explore all these different types of insurance:

Personal Insurance Policies:

1. Life Insurance: Life insurance is a very useful financial tool that basically indemnifies your family in case of your death. It is a contract, in the form of a policy, between two parties where one party insures the other party that in case of the latter party’s death the latter’s family will be given a particular sum of insured money.

Life insurance offers financial protection to you and your family. These days some plans also offer optional add-ons, such as critical illness benefits, accidental death benefits, and more. The importance of life insurance should never be ignored in ensuring the financial safety of your close ones.

“Should I buy Life Insurance?”

Yes, you should definitely buy Life Insurance as it saves your family from a possible financial crisis that could occur due to your fatality. And it is a smart financial decision to make. Plus it puts your mind at ease.

Are you still thinking about buying life insurance? Before you wait anymore, allow us to tell you that life insurance premium gets expensive as you age. So think before you keep waiting.

“What are the factors that affect life insurance?”

The premium amount for your life insurance depends on a number of factors. Some of these have been mentioned below:

Age: Age is one of the core factors that impact the amount of life insurance premium. Because as you start growing old the chances of insurer paying the claim increase. This is the reason behind the increase in the price.

Gender: As it is commonly known, women live longer than men and this is the reason why women pay lower life insurance premiums.

Present health and medical history: You need to undergo a medical test before purchasing a life insurance policy so that the insurer can assess your health status but in some cases insurance companies might not ask you for the same, especially if you’re young.

Though, having a history of medical issues will hike the premium for life insurance. Family health history and hereditary diseases also do the same.

Lifestyle: If you smoke, drink, or make any other poor lifestyle choices then these increase the risk of you getting prone to medical conditions. Which is the reason why it impacts the premium amount for a life insurance plan.

What do I need to present to file a claim for life insurance?

- Claimant statement form

- Death certificate in case of death claims

- Medical papers, diagnosis reports, and other necessary documents

- ID proof, residential address proof and cancelled cheque or a copy of bank passbook entry

- And the claim settlement team will assess your claim and get back to you if they need any more information.

2. Health Insurance: In India, A health insurance policy, also called medical insurance, covers Hospitalization & some day care procedures as payment of your medical bill amount to the medical care provider directly on your behalf or reimbursement to you once you have made the payment to the medical care provider.

Health Insurance in India indemnifies the insured primarily for hospitalization. This means you must be admitted to a hospital for at least 24 hours to avail of policy benefits. Along with that due to advancements in technology certain procedures which take less than 24 hours, called daycare procedures are covered.

Many policies also cover the cost of medications & ambulance charges also these days.

Here’s an interesting fact about Health Insurance. While a health insurance plan protects you financially against all diseases. It also helps you boost tax savings. Under section 80D of the Income Tax Act, 1961, you can claim tax benefits against your health insurance premium.

What are the benefits of buying health insurance?

- Covers pre and post hospitalization

- Provide cashless treatment

- Lets you claim tax benefit

- Provides no claim benefits

Things to consider before exploring or buying health insurance

- First of all, take a look at all the plans and choose one that is best as per your requirement

- You need to look for payment options and see what options are available

- Before purchasing a health insurance plan, see whether your policy covers pre-existing illnesses or not. Because there are certain medical conditions that are not covered in some policies.

- Check the list of hospitals thoroughly and make sure that the nearest hospital is mentioned. Ensure your nearest hospital is on the list.

3. Motor Insurance:

Insurance for four-wheelers, commercial trucks, two-wheelers, and other road vehicles is called Motor Insurance. J Insurance provides financial protection in case of physical damage and covers for natural calamities and any loss or damages sustained by the policyholder due to an unfortunate and unforeseen event.

Motor insurance is mandatory for all two-wheeler and four-wheeler vehicles such as cars, bikes, scooters, and trucks that are plying on the roads in India. Vehicle owners can avail motor insurance even for commercial vehicles as well.

Features of Motor Insurance:

A Motor Insurance policy comes with a suite of features that come with a set of benefits for the policyholders. Here are some of those features that you should know about:

You can add or remove any particular add-on as your requirement.

Motor insurance not only provides cover for the damages caused by an accident but also covers you from theft, natural calamity, fire damage, vandalism, disasters, etc.

You can get the benefits of a cashless claim by providing enough evidence in case of accidents and theft.

Motor insurance also provides a no-claim bonus feature. Under this feature, if you do not raise a claim during the policy tenure then the insurer will provide you with a specified discount either on the premium or on purchasing any other add-on. It varies from insurer to insurer.

Insurance companies keep on coming up with different plans and add-ons to provide you better coverage as well as provide assistance in case you get stuck during the claiming process.

Commercial Insurance Policies:

1. Standard Fire and Special Perils: Standard fire insurance protects your property and assets from unseen mishaps like fire, earthquake, storm, flood, riots, etc. Standard fire insurance can also be coupled with burglary and theft insurance.

Key things to note about SFSP:

- SFSP policy can be taken by owners of both residential and commercial properties.

- The policy covers contents of the building such as household goods, furniture, machinery, electrical fittings and stock.

- Generally referred to as the Fire policy in the market, the policy covers various other events like explosions, natural calamities and riots.

- The standard coverage can be enhanced with Add-On covers on payment of an additional premium.

- Long-term policy available with discounts for individual house owners

- Comprehensive coverage for Commercial/Industrial organizations is available

- Facilities like Floater Policy, Declaration Policy and Floater Declaration Policy are available for stock.

Discounts for the availability of safety features like fire extinguishing appliances and for favorable claims experience.

Risks covered under SFSP:

- Fire

- Lightning

- Aircraft Damage

- Explosion/Implosion

- Riot, Strike and Malicious Damage

- Tempest, Hurricane, Tornado, Flood, Storm, Cyclone, and Typhoon

- Impact Damage

- Subsidence and Landslide including Rock slide

- Overflowing and rupture of tanks

- Missile Testing operations

- Leakage from Automatic Sprinkler Installations

- Bush Fire

Exclusions

- War and Nuclear Perils

- Any loss that’s not covered as an insured peril and is caused by pollution or contamination of some sort

- Loss, destruction or damage to the stocks in Cold Storage premises caused by the change of temperature (This can be availed via Deterioration of stock policy) Deterioration of stock insurance includes damage to goods stored in the aforementioned cold storage space, that occurs mainly due to a break down of the cold storage plant resulting in the change of temperature and therefore damage to the goods

- Loss by burglary or theft (can be availed as add on)

- Removal of property to other sites

- Consequential or indirect loss (can be availed via FLOP-Fire consequential loss of profit)

- Any loss or damage that has been caused by retardation, interruption, or operation of any kind is not covered among the perils covered.

2. Travel Insurance/Overseas Mediclaim: Falling ill in a country which is not your own is an invitation to double trouble. As it is said sickness or accidents are never warned before they occur. One should always be prepared to tackle any of these situations. And nothing beats travel insurance in doing that.

Studying abroad is expensive. Other than all the budgeted expenses, you may face some unpredictable ones as well.

To make sure that such expenses do not burn a deep hole in your pocket, and hinder your higher education, get a travel insurance policy specially tailored for students.

Coverages under a Travel Insurance Policy?

- Sponsor protection

- Missed Connections / Missed Departure

- Fraudulent Charges (Payment Card Security)

- Personal liability

- Hijack cash benefit

- Baggage Covers

- Checked Baggage Loss

- Checked Baggage Delay

- Loss of passport

- Bail bond

Medical

- Maternity benefit

- Cancer screening and mammography examinations

- Physiotherapy

- Sickness Dental Relief

- Childcare benefits

- Accident & Sickness Medical Expenses Reimbursement

- Accidental death and dismemberment 24 Hours

- Repatriation of remains

- Tuition fee reimbursement due to sickness in the middle of the term or due to death of the insured

- Visit by an immediate family member under certain conditions paid

- Emergency Evacuation

Exclusions

- Any loss of baggage sent in advance or anything shipped separately

- Any baggage delay when you’re in India is not covered.

- Any flight delay due to a hazard made publicly known prior to purchase of Policy.

- Rock climbing, scuba diving, and paragliding. All the adventure activities such as these are also not covered

- Losses arising from intoxicated behaviour

- Local agitations and protests

- Losses sustained during a nuclear attack or radiation leak

- Self-harm

3. Marine Insurance: Marine insurance policy, as the name suggests, covers the loss or damage of cargo of any kind transported through sea,air, rail, or road.

Cargo insurance is the sub-branch of marine insurance, though Marine insurance also includes Onshore and Offshore exposed property, (container terminals, ports, oil platforms, pipelines), Hull, Marine Casualty, and Marine Liability.

When goods are shipped through mail or courier.

Types of Policies

Marine Specific: It is for a specific voyage only.

Marine Open: Marine Open insurance policy is for business owners who do regular deliveries and don’t want to deal with the regular hassle of insurance-related documentation and waste their time issuing new policies every day, calls for a Continuous Insurance Cover, which is Marine open Cover. Here Sum Insured is a prospective value that may be incurred in a year, & after every voyage deductions are made from Sum Insured.

Marine STOP policy: In the marine STOP policy your premium is calculated and charged based on your sales turnover. STOP Provides You Coverage On: Imports + Customs Duty (Actual Or Deemed / Contingent) + Domestic Purchase Of Raw Materials, Consumables & Stores + Any Number Of Inter- Factory / Inter-Depot / To & Fro Job Worker Movements + Exports (FOB/CIF) + Domestic Sales Of Finished Goods Temporary Storage Cover At Intermediate Locations Like Job Workers / C & F Premises Etc.

Valuation & Terms of Sale Valuation of Sum Insured & Terms of Policy are determined also by Terms & conditions between buyer & seller. A valuation can be consignment value only, C Or Consignment value plus 10 per cent, C+10% Or Consignment value, Insurance value & Freight, CIF Or Consignment value, Insurance value, Freight plus 10 per cent, CIF+10% On basis of TnC between seller & buyer cover could be FOB or Free on Board, warehouse to warehouse, ending at the port of discharge etc.

4. Engineering Risk: The Engineering Risk Insurance provides a comprehensive insurance solution covering a wide range of risks to which an Engineering project is exposed, starting from the construction to the whole tenure of the project.

Types of Engineering Risk policies

Contractor's All Risk Insurance policy offers comprehensive coverage against damage or loss in respect of construction plant, contract work, construction machinery and/or construction equipment.

- This policy is specifically designed for architects, construction engineers and financiers because it provides sufficient financial protection to all the parties that are involved.

- The projects that are covered in most of the policies are civil engineering on condition that the civil work is more than 50% of the total value of the contract,

Here coverage begins from the time the material is taken in to store and goes on during the construction and prevails till the time when the project is handed over.

What risks does your policy cover?

Material Damage: Under this loss, damage or destruction of property incurred due to any cause other than those excluded in policy are covered. The amount that this policy is a good certain amount that nears the limit usually, but will not exceed the limit that is assured by the policy.

Third-Party Liability: Legal liability related to accidental damage or loss caused to property of a third person or fatal or non-fatal injuries caused to a third person.

Perils covered generally are:

1. Fire & allied perils

2. Collapse

3. Earthquake, shock & fire

4. Faults in construction

5. Storm, tempest, flood, Inundation, Cyclone

6. Negligence & human error.

7. Water Damage

Erection All Risk

What risks does your policy cover?

Erection All Risks is a complete comprehensive insurance package for plant and machinery and other construction-related damages. This policy can be extended to include third-party liability related to work conducted on the contract site.

Exclusions:

- Nuclear reaction, Nuclear radiation or Radioactive contamination

- The willful act or willful negligence of the Insured or of his responsible representative

- Cessation of work whether total or partial

- Inventory losses

- Manufacturing / design defects

- Consequential loss

Contract Plant and Machinery:

The toughest job on any construction site is done by the tools and equipment. From hauling and moving materials to excavate earth and debris, generation of power, etc., round the clock – it’s all done by machinery.But what happens when big machinery stops working?

The contractor’s Plant and Machinery insurance policy is a stress-free way to protect your expensive construction machinery and handle its repair costs.

What risks does your policy cover?

All the heavy machinery that aids the construction projects is covered under this policy. For eg: Bulldozers, cranes, excavators, compressors, etc. Any damage due to an accident arising out of external perils is also provided for.

The policy is applicable when the machinery is at work or even if it is at rest. Plus, it also prevails when the machinery is dismantled to transport.

Exclusions

- Any failure which is electrical or mechanical in nature is not covered.

- Pre-existing defects do not get covered.

- Defective lubrication or lack of oil or coolant.

- Any sort of damage for which the manufacturer or supplier is responsible.

- Any consequential loss.

- Any damage that has been caused due to common use like moving it on road except construction.

- Workmen Compensation Insurance

- Workmen’s Compensation insurance is a tool by which an employer demonstrates the ability to satisfy the obligations imposed by the worker’s compensation act.

Why do you need a Workmen Compensation Policy?

The Workmen's Compensation Insurance Policy or WC Policy provides for coverage for compensation to your employees as deemed mandatory by the Workmen's Compensation Act of India, monitored by the Ministry of Labor, for bodily injury or death caused due to accidents / occupational diseases arising out of and in the course of employment.

This product is addressed to:

- All manufacturing companies with employees who fall under the purview of the Workmen's Compensation Insurance Act, 1923.

- All business organizations who have Employers' Liability exposures under Common Law.

What risks does your policy cover?

Workmen Compensation Policy provides Indemnity to the insured against his liability as an employer to accidental injuries, both fatal and non-fatal, sustained by the workmen during work.

An extension is available on extra premium-medical surgical and hospital expenses including the ambulance charges to the hospital for accidental employment injuries.

Liability for diseases sustained due to the nature of work at the site, as mentioned in Part C / schedule III of the Workmen Compensation Act are called Occupational diseases, on additional premium; that arise out of and in the course of employment.

The amount of compensation is calculated as per the provisions of WC Act.

However, the policy will not compensate in the following conditions:

- Any injury not resulting in a fatality or partial disablement for a period extending 3 days

- The initial 3 days of disablement where the total disablement turns out to be less than 28 days

- Any non-fatal injury sustained due to an accident which is directly attributable to (a)Influence of drinks or drugs (b)Willful disobedience of an order for securing the safety of the workmen © Willful act of removing or disregard of safety gear.

- Group of perils happening due to war and nuclear attacks

- Unless it is specifically declared. Any liabilities to employees or contractors of the insured are also not covered.

- An employee who is not a "workman" as per the Workmen Compensation act.

- Any occupational diseases (which occur due to the nature of the work) and are mentioned in part "C" of schedule III of the Workmen Compensation Act, unless the cover is extended on an extra premium.

Any Increase due to any change in the statute provisions after the policy had been incepted provided it is below one statute/one forum for the same injury.

Group Medical Coverage

A group insurance policy is really a good tool that lets employers provide the advantage of providing standardized medical coverage and avail the same at very competitive premium rates.

You can avail of group insurance policies for a group that you manage or own. Groups – in this context can be employer-employee groups or non-employer-employee groups as defined by IRDA’s group insurance guidelines.

(Some of the examples are holders of the same credit card, savings bank account holders of a bank or members of the same social or cultural association and so on. All these groups can avail Group Medical Coverage)

Here are some things to be careful about when you participate in a group policy :

- The policy is issued in the name of the company and accepted by the manager on behalf of the organization

- You should receive a certificate of insurance if you participate in a non-employer-employee group plan.

- This certificate should contain

- the time horizon of the benefits

- premium charges and related information

- &nb